Every year, governments lose substantial corporate tax revenues as multinational corporations shift profits to low-tax jurisdictions. In response, two parallel international reform processes have emerged to address the weaknesses of global tax governance. The first, led by the OECD/G20, resulted in a 15 percent global minimum tax (known as “Pillar Two”), designed to curb profit shifting and to stabilise corporate tax competition.

The credibility of this process isincreasingly challenged by country-specific carve-outs, uneven implementation, and geopolitical tensions – particularly vis-à-vis the US. At the same time, many developing countries have criticised the OECD/G20 process as insufficiently inclusive and overly dominated by advanced economies. In response, several states have advanced a parallel reform effort within the UN, where negotiations on a Framework Convention on International Tax Cooperation are now underway.

These fragmented, parallel processes create a strategic dilemma for the EU. As one of the earliest and most comprehensive implementers of Pillar Two, the EU has played a central role in making the global minimum tax politically credible. At the same time, it faces pressure to engage constructively in the emerging UN process, which promises greater inclusiveness but uncertain enforceability. How the EU positions itself between these two tracks will shape not only the future of Pillar Two, but the broader architecture of global tax cooperation.

This policy brief addresses the following central policy question: how should the EU navigate both the OECD and UN reform processes to preserve effective and legitimate global tax governance? We argue that the EU must act as a stabilising force by defending the substantive enforcement of the 15 percent minimum tax, resisting the urge to use carve-outs and formal compliance loopholes both within and outside of the EU, and engaging strategically in the UN negotiations to encourage greater inclusiveness while preserving effective enforcement.

Addressing Profit Shifting: A Fragmented Approach to Global Tax Reform

The current reform landscape builds on a decade of efforts to address profit shifting by multinational enterprises. In 2013, the OECD/G20 developed the Base Erosion and Profit Shifting (BEPS) project meant to combat corporate tax avoidance. The BEPS project improved transparency but did not fundamentally alter incentives for tax competition. Growing tensions over digital taxation and unilateral policies in the form of Digital Services Taxes pushed governments toward a more comprehensive solution, culminating in the 2021 Two-Pillar Solution. Pillar Two, the global minimum tax, emerged as its most concrete outcome and marked the first serious attempt to establish a coordinated floor for corporate taxation.

OECD/G20: Global Minimum Tax via Pillar Two

At its core, Pillar Two rests on an innovative and strategically designed logic, which bypasses the need for universal consensus. Instead of requiring every tax jurisdiction to adopt a 15 percent minimum corporate tax rate, Pillar Two changes incentives by allowing other countries to tax undertaxed profits if a certain jurisdiction chooses not to implement the rules. This means that not adopting this tax regime does not protect low-tax advantages; it merely shifts taxing rights elsewhere. This clever ‘backstop’ design reduces the gains from defection and makes participation the rational choice for many governments. Empirical research suggests that implementation by the G7 and the EU alone would be sufficient to secure much of the regime’s effectiveness, given that most large multinationals either have major operations or their headquarters located in these economies. In this respect, the EU’s early adoption of Pillar Two under Council Directive 2022/2523 has played a pivotal role in making the reform politically credible and in triggering broader uptake.

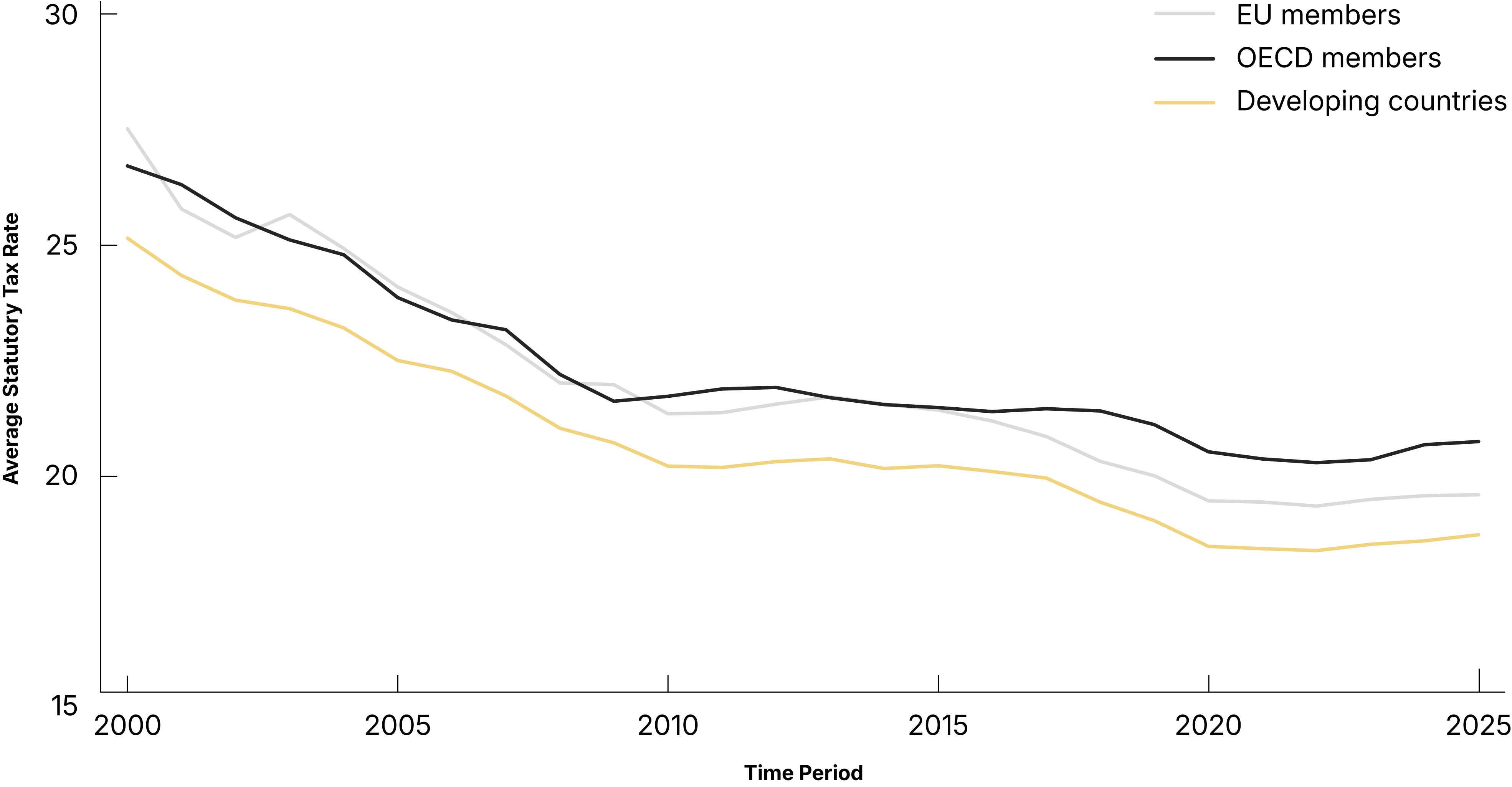

Figure 1: The Fall of Corporate Statutory Tax Rates After 2000

Source: Authors based on OECD Corporate Tax Statistics.

Figure 1 shows that since Pillar Two was announced, statutory corporate tax rates have stopped decreasing. However, while effective, its strategically designed logic also makes the reform vulnerable. Pillar Two’s effectiveness depends on sustained political commitment by key players and on limiting exemptions, carve-outs, and purely formal compliance. The US continues to stress national tax sovereignty and seeks avenues to circumvent common rules through its unilateral system. Other actors have responded by accommodating US demands through carve-outs, culminating in the 2026 “side-by-side” package. Many observers believe this development undermines Pillar Two’s integrity and paves the way for similar carve-outs elsewhere. At the same time, governments began exploring ways to comply with the rules in form rather than substance, for example by introducing their own domestic minimum taxes or redesigning tax incentives. In practice, this risks countries remaining formally aligned with Pillar Two while continuing to preserve relatively low effective taxation and competitive advantages for multinational firms. While Pillar Two changed the global conversation on corporate taxation, its long-term effectiveness remains uncertain.

The Early Promises of the UN-Led Negotiations

Dissatisfaction among developing countries with their degree of influence within the OECD-led tax reform process has led some of them to shift reform efforts to the UN. Although the OECD/G20 Inclusive Framework, a negotiation platform involving over 140 jurisdictions and responsible for developing the BEPS-related reforms, expanded formal participation, many governments perceived agenda-setting power as concentrated among major economies. In 2023, the UN General Assembly launched negotiations on a Framework Convention on International Tax Cooperation, signalling the emergence of a second, parallel rulemaking processon global tax.

The UN negotiation process prioritises issues such as the taxation of cross-border services in a digitalised economy and tax dispute resolution. Its ‘one-country-one-vote’ structure enhances formal inclusiveness, and most developed countries – including EU member states – are continuing to participate, despite US disengagement. However, the institutional trajectory remains uncertain. It is unclear whether the negotiations will produce binding and enforceable standards. What is more, parallel rulemaking risks duplication or divergence from OECD frameworks. The result is therefore not a shift from one forum to another, but the coexistence of two competing, but partially overlapping, centres of global tax governance with different institutional logics. For the EU, this fragmentation creates a strategic challenge: disengagement from the UN process risks marginalisation, but uncritical alignment risks weakening the coherence and enforceability of global tax governance.

Strengthening Tax Governance: A Strategic Dilemma for the EU

The EU now faces a strategic policy dilemma: how to preserve the integrity of the OECD-led global minimum tax while constructively engaging with the emerging UN tax process without allowing fragmentation, geopolitical pressure, or symbolic compliance to hollow out reform? The EU is not a neutral observer in either forum. It has invested heavily in OECD-led tax cooperation, including Pillar Two, and its early implementation was decisive in making the global minimum tax politically credible. In the UN process, however, the EU has taken a more cautious and strategically neutral position, participating in the negotiations but avoiding full alignment with either rejection or unqualified support. Furthermore, while formal implementation of global minimum tax is largely in place, ensuring consistent and substantive application across EU member states – and limiting the use of design flexibilities that weaken effective taxation – remains an ongoing challenge even within the EU.

In the UN negotiations, the selection of tax-dispute resolution as the second protocol was widely interpreted as a concession to EU and other developed-country concerns. The EU, therefore, possesses significant, though not unlimited, leverage. While individual member states may struggle to shape outcomes alone, coordinated EU action can play a stabilising role, particularly by resisting unilateral pressure from the US and by engaging strategically with the opportunities presented by the UN negotiations. The central question is thus not whether the EU can shape outcomes, but how it should use its influence to safeguard coherence and effectiveness in global tax governance under increasing geopolitical strain.

The EU and the OECD Tax Cooperation Process

Despite the hurdles now facing Pillar Two, the EU has remained a consistent advocate for a global minimum tax, presenting it as a central tool for financial development and a reform that should be adopted globally. The G20 has also reaffirmed its commitment to continued engagement with Pillar Two during its latest summit in November 2025. Nevertheless, if the EU wants to prevent the fragmentation of the global minimum tax reform, it must address three main issues.

First, the EU must address the growing normalisation of country-specific carve-outs that accommodate powerful states at the expense of the regime’s integrity. The US has become the key pressure point. In early 2025, threats of US retaliation led to a ‘side-by-side’ arrangement that recognised the US minimum tax (in addition to Pillar Two) and exempted US multinationals from key backstop rules. While this preserved participation, it weakened enforcement symmetry and set a precedent for further exceptions. Persistent doubts remain over whether US firms will consistently face an effective 15 percent tax burden, as the side-by-side arrangement reduces the exposure of US multinationals to key Pillar Two mechanisms.

The EU has remained a consistent advocate for a global minimum tax.

For the EU, ensuring that US multinationals are indeed subject to the same 15 percent tax floor must be a central priority – not only to safeguard the credibility of Pillar Two, but also to protect the competitiveness of EU-based firms. While early EU implementation of Pillar Two triggered adoption elsewhere by raising the risk of foregone revenue for non-adopting states (as illustrated by Brazil’s decision to implement the reform), a permissive approach toward US exemptions would weaken incentives for compliance, invite further demands for special treatment, and ultimately undermine the global minimum tax itself.

Second, the EU should actively limit the spread of non-substantive formal implementation of Pillar Two, both within the EU and internationally. Because Pillar Two is not a minimum standard, many governments formally endorse the 15 percent floor while adapting the rules to domestic preferences and administrative simplicity, rather than ensuring substantive alignment. This flexibility has opened new loopholes: by redesigning tax incentives, countries can remain formally compliant with Pillar Two while preserving de facto low effective tax rates.

To illustrate: Pillar Two does not prohibit incentives outright but privileges instruments such as grants and refundable tax credits, which fiscally stronger states can more easily afford. Ireland’s conversion of Research and Development deductions into refundable credits and similar reforms underway in the United Arab Emirates show how both EU and non-EU jurisdictions can protect status quo tax-competition strategies while remaining formally compliant with the new tax regime.

Rather than attempting to displace the UN process with the OECD track, the EU should prioritise coordination between forums.

Empirically, the trend of formal compliance is significant: of the 21 countries that have enacted a global minimum tax, 13 have opted for domestic minimum taxes rather than the OECD’s qualified rules. The EU’s common legal framework under Directive 2022/2523 has helped establish early and coordinated implementation across member states and has limited some forms of regulatory divergence. However, because the Directive largely reproduces the flexibility embedded in Pillar Two itself, it has not fully prevented the emergence of incentive-driven compliance strategies within the EU itself. The effectiveness of Pillar Two depends not only on broader international adoption, but also on the EU’s willingness to ensure consistent and substantive enforcement among its own member states. Beyond its borders, the EU should promote comparable standards internationally and resist the normalisation of formally compliant but economically hollow implementation practices.

Third, the EU should strengthen developing-country participation in the OECD process while accepting the reality of the UN-led tax initiative. Enhancing inclusiveness within the OECD framework is essential to reducing institutional rivalry and preventing further fragmentation of global tax governance. Rather than attempting to displace the UN process with the OECD track, the EU should prioritise coordination between forums and work to minimise agenda duplication.

The EU and the UN-Led Process

While the OECD track requires the EU to strengthen implementation and inclusiveness, the UN process presents a different challenge: how to engage constructively in a more representative forum while preserving coherence in global tax governance. Internal EU constraints rooted in national tax sovereignty have also been even more visible in the UN negotiations, where the fragmentation of member state positions contributed to EU abstention and reinforced perceptions of the EU as reactive rather than agenda-setting. Despite these tensions, participants in the UN process have generally sought to keep the EU engaged and have left considerable space for constructive cooperation. This is reflected in the decision to prioritise (comparatively) less contentious issues, such as tax dispute resolution, where opportunities for consensus are greater than in more politically sensitive areas of international taxation.

For the EU, the UN process offers a strategic opportunity to rebuild trust with developing countries. Even limited outcomes focused on capacity building, administrative cooperation, and best-practice exchange respond to a clear demand for more democracy and can deliver tangible benefits. Stakeholders consistently identify EU support for technical assistance and institutional capacity as particularly valuable, suggesting that sustained engagement would strengthen both the legitimacy and practical impact of the negotiations.

The strategic challenge is not how to choose between the OECD and the UN, but how to remain actively engaged in both processes.

Although several developed countries voted against the initial UN resolutions, most have continued to participate constructively, with the notable exception of the US. US disengagement has, paradoxically, reduced geopolitical blockage and enabled more cooperative dynamics among remaining participants. At the same time, significant uncertainties persist. While the UN forum enhances the participation of states, doubts remain about implementation capacity and financial sustainability. Moreover, the two-thirds majority voting rule gives developing countries the ability to shape substantive outcomes, potentially diverging from OECD standards.

For the EU, the strategic challenge is not how to choose between the OECD and the UN, but how to remain actively engaged in both processes, strengthening substantive enforcement within the OECD framework while constructively shaping the inclusiveness and legitimacy of the UN track. In an increasingly fragmented and geopolitically contested tax environment, the EU’s role is ultimately less about defending a single institutional forum than about preserving coherence, credibility, and effective cooperation across the emerging architecture of global tax governance.

ENSURED Report Citation:

Boukal, Tomáš, Petr Janský, Miroslav Palanský, and Michal Parízek. 2025. “Reforming Global Tax Governance: OECD and UN Paths to Effective and Participatory Tax Reform.” ENSURED Research Report 16 (November): 1-18. https://www.ensuredeurope.eu.

.png)